In 2025, simply holding onto your crypto is no longer the end game. With the rise of decentralized finance, investors are learning how to make their digital assets work for them through crypto lending. Whether you are a long-term holder of Bitcoin or Ethereum, or just entering the space, monetizing your crypto has become an accessible strategy for passive income, but the path you choose matters greatly.

At the heart of crypto lending lies a simple idea: just like you earn interest on a bank deposit, you can earn returns by lending your crypto assets. This has led to two major approaches: Centralized Finance (CeFi) and Decentralized Finance (DeFi). Both offer opportunities to generate income, but they differ in control, risk, and transparency.

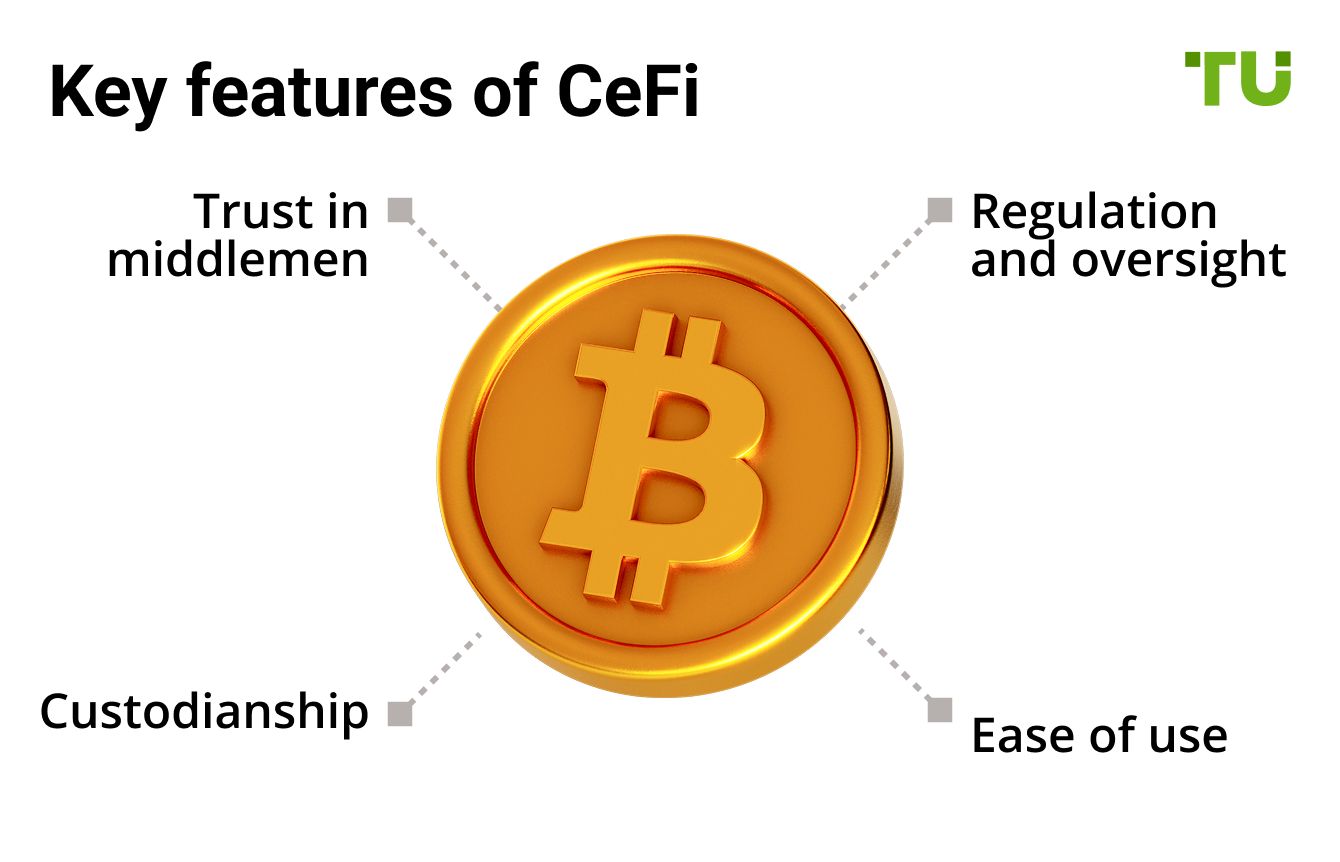

Let us begin with CeFi, the familiar model. Think of platforms like Coinbase, BlockFi (before its collapse), or Celsius. These companies act like crypto banks. You lend your Bitcoin or stablecoins to them, and they lend it further to borrowers. In return, you earn a fixed interest rate, and the platform handles everything else. The catch? You are handing over control of your asset. If that company fails due to mismanagement, hacks, or regulatory issues, you could lose your funds. This risk was made painfully clear when several major CeFi players crumbled following the 2022 crypto crisis, taking billions of customer funds with them.

DeFi changes the game. With platforms like Aave, Compound, and MakerDAO, everything runs on smart contracts — self-executing code on the blockchain. There is no company, no CEO, no gatekeeper. You interact directly with the protocol, which holds your assets securely in a smart contract and pays interest in real time. Want to borrow crypto? You will need to deposit more than you borrow, a concept called overcollateralization. This protects lenders in case of default. If the value of your collateral drops too much, the system automatically liquidates it to repay the loan.

Here is how it works in practice: let us say you have 1 Ethereum and want to earn passive income. You deposit it into Aave. Other users borrow that Ethereum by posting collateral, and you receive a yield based on real-time market demand. Your funds never leave the smart contract, and you can withdraw them anytime. No bank involved, no human decisions, just code.

While DeFi offers unmatched transparency and control, it is not without risks. Smart contracts can have bugs. Protocols can be exploited. And market volatility can trigger sudden liquidations. But unlike CeFi, where your asset is only as safe as the company holding it, DeFi platforms offer a more trustless model, one where the system works even if you do not trust the people behind it.

So, how should you begin?

-

Start small. Use trusted DeFi platforms like Aave or Compound to lend stablecoins like USDC or DAI.

-

Understand the risk of liquidation. If you are borrowing, monitor your collateral closely.

-

Never chase high returns blindly. Yield that sounds too good to be true often comes with extreme risk.

-

Keep your funds in your control. Use decentralized wallets like MetaMask for interacting with DeFi.

The next wave of wealth creation will not be about trading alone. It will be about putting idle assets to work. Whether you choose CeFi for simplicity or DeFi for full control, the future of passive income in crypto is already here. And for those who move early and wisely, the rewards can be substantial.

For more simplified financial insights and crypto tools that help you grow wealth smartly, follow You Finance on Instagram and Facebook. We decode modern money one post at a time.